Overcoming The Barriers To Global Biosimilar Adoption

By Ravi Limaye, Biocon

This article will be part of the CPhI 2016 Annual Report, which will be released during the CPhI Worldwide event in Barcelona (October 4-6, 2016).

The ability of biologics to target specific proteins makes them more effective treatments than small molecule therapies for a variety of medical illnesses and conditions. Biologic therapies such as insulin, erythropoietin, and growth hormones have played an invaluable role in treating serious illnesses such as diabetes, anemia, and renal diseases. More complex biologics like monoclonal antibodies (mAbs), cytokines, and therapeutic vaccines are now transforming the standard of treatment for cancer, autoimmune disorders, and other chronic diseases. It is expected that by 2020, new biologic treatment options will be available for conditions like severe asthma, chronic eczema, atopic dermatitis, and familial hypercholesterolemia across developed markets.1

Cancer immunotherapies, which harness the power of the immune system to target and fight malignant tumors, are expected to revolutionize cancer treatment by sparing patients the toxic effects of chemotherapy.

Biologics Landscape: 2020

The global biologic drug market will top $390 billion by 2020, accounting for nearly a third of the global pharmaceutical market by value.2 The increasing penetration of biologics will, in turn, lead to higher demand for biosimilars, or follow-on versions of original biologics, in the global pharmaceutical market. Since the first biosimilar approval in the European Union (EU) in 2006, there are now several hundred biosimilars approved globally.3 By 2020, biosimilars have the potential to enter markets for a number of key biologics that have current sales of more than $50 billion annually.2 With the approval of the first biosimilar in the US in 2015, and the expected patent expiration of 12 biologics by 2020, estimates suggest that the global biosimilars market could reach $25billion to $35 billion by 2020.4

Access and Affordability

Globally, we are witnessing the rapid spread of a pandemic of noncommunicable diseases (NCDs). It is estimated that 38 million people succumb to NCDs like cancer, diabetes, cardiovascular diseases, and chronic respiratory disease annually. Today, cancer is the cause of one in seven deaths worldwide,5 while diabetes now affects nearly one in 11 adults globally.6

Biologics like insulins and monoclonal antibodies have emerged as a class of highly effective, transformational, life-saving drugs targeted at chronic diseases like diabetes and cancer. The high cost of biologic therapies, however, pushes them out of the reach of many patients, especially those in low- and middle-income countries (LMICs) — like India, where drug regimens can cost several months’ wages, making the treatment of chronic disease simply unaffordable.

This large unmet need can only be addressed through high-quality, affordable biosimilars that provide cost-effective alternatives to expensive reference biologics. Biosimilars offer patients, physicians, and payers a wider option of treatment choices, as they compete with original biologic medicines across a growing range of therapy areas.

The imperatives to improve health care access and reduce the cost of care present growth opportunities for biosimilar manufacturers in both emerging and developed markets. According to investment research organization Sanford C. Bernstein & Co., 70 programs are now in clinical trial stage or later, with 11 approvals in EU, three in the U.S., and 44 programs in pivotal trials.7 This is likely to result in a highly competitive marketplace over the next five years. The cumulative potential savings to health systems in the five major EU markets and the U.S., as a result of the use of biosimilars, could exceed $55 billion in aggregate over the next five years, and eventually reach as much as $111 billion.2

The experience of the European medical community has been positive in the 10 years since the approval of the first biosimilar in the EU. The use of erythropoietin, granulocyte-colony stimulating factors, and human growth hormone have all increased in this period, driven by the availability of biosimilars as well as factors such as expanded indications.2 Going forward, insulins and monoclonal antibodies are also expected to experience similar uptake as biosimilar versions become widely available. Infliximab, the first biosimilar mAb to be approved by the European Medicines Agency (EMA) in 2013, was offered to patients in Europe at a deep discount of nearly two-thirds the price of the innovator product. Since then, Norway, Denmark, and Finland have achieved a near total switch to biosimilar versions of Infliximab.8

Biosimilars and Developed Markets

Developed markets such as the U.S., EU, and Japan offer strong growth opportunities for biosimilars manufacturers. As governments in developed markets like EU and Japan strive to rationalize healthcare spends, they are encouraging the entry of high–quality, yet affordable, biosimilars through dedicated regulatory pathways and stringent, abbreviated approval processes.

Biocon, through its partner Fujifilm Pharma, recently launched insulin glargine in Japan. This product is the first biosimilar from India and second biosimilar insulin glargine to be approved in Japan. Industry guidance on biosimilars was released by Japan’s Ministry for Health, Labour and Welfare (MHLW) back in 2009. Nine biosimilars were approved in Japan between 2009 and 2016, according to Generics and Biosimilars Initiative (GaBI).

In fact, developed markets continue to have the highest number of biosimilar molecules in development — estimated at 29 in Europe, 19 in the U.S., and seven in Japan.9

Biosimilars and Emerging Markets

High out-of-pocket costs for medicines in emerging markets means physicians are more open to prescribing low-cost alternative therapies. In India, a Deloitte survey found that physicians were willing to prescribe a first-line critical therapy if it was offered at a 60 to 70 percent discount. In China, getting on the essential drugs list means mandatory usage by many hospitals; however, it also comes with price cuts of 25 to 50 percent.10 This offers a huge potential opportunity for biosimilar manufacturers committed to develop high-quality, yet affordable, world-class biosimilars. Emerging markets including the BRICS (Brazil, Russia, India, China, and South Africa) and MIST (Mexico, Indonesia, South Korea, and Turkey) provide the best future opportunity for manufacturers of biosimilars.5

India saw the launch of its first biosimilar back in 2003, when Dr. Reddy's Laboratories launched biosimilar rituximab at half the price of the innovator product, which is used to treat certain kinds of cancer and autoimmune diseases such as rheumatoid arthritis. A year later, Biocon introduced an affordable recombinant human insulin product that enhanced patient access to insulin across India, resulting in improved diabetes management. Since 2008, the Indian biosimilar industry has been growing at a compound annual growth rate of 30 percent. There are approximately 25 Indian companies operating in the biosimilar space, marketing close to 50 products in the Indian market.11 Today, Indian patients have access to biosimilars like insulins, insulin analogs, filgrastim, trastuzumab, and adalimumab, among others.

This early experience with developing biosimilars is paving the way for Indian players to capitalize on the unfolding global opportunity. Indian pharma companies have expanded their pipelines to include biosimilars, as top-selling biologics go off-patent worldwide.

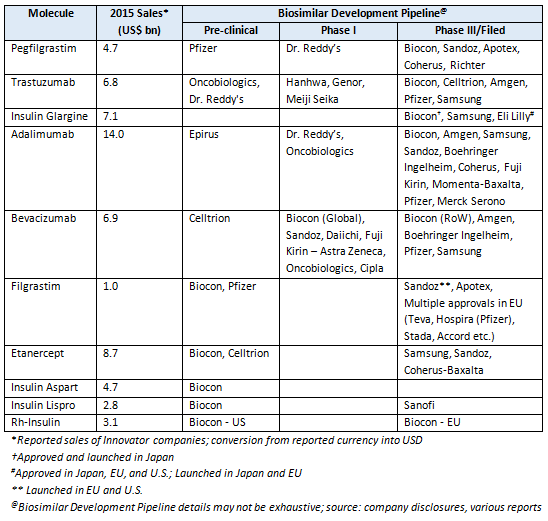

Biocon, in partnership with Mylan, is developing a portfolio of six biosimilars for oncology and autoimmune indications (trastuzumab, pegfilgrastim, adalimumab, bevacizumab, etanercept, and filgrastim) and three generic insulin analogs (Glargine, lispro, and aspart). The two companies recently moved a step closer to enabling access to these drugs in developed markets after the EMA accepted for review the marketing authorization applications (MAAs) for two of their biosimilars, pegfilgrastim and trastuzumab.

India, which first issued biosimilar guidelines in 2012, recently announced updated draft guidelines for biosimilars. The 2016 Guidelines on Similar Biologics incorporates high-end analytics and clinical science to abbreviate the development pathway. However, while the timelines may be compressed for marketing authorization, the emphasis is on a science-led regulatory pathway that delivers safe and efficacious biosimilars with comparable clinical and immunogenic profiles. Additionally, there is a post-marketing pharmacovigilance plan to monitor safety, efficacy, and immunogenicity in a real-use setting, which truly differentiates these guidelines.

In addition to India, many other emerging market countries have either defined biosimilar approval pathways or are finalizing guidelines. South Korea published biosimilars guidance in 2009, while China unveiled them in 2015. In Latin America, several regulatory authorities such as ANVISA in Brazil, COFEPRIS in Mexico, and ANMAT in Argentina have developed their own biosimilar regulatory abbreviated pathways.12

Evolution of Global Biosimilar Regulations

Global regulations and guidelines need to evolve if biosimilars are to make as much of an impact as small molecule generics have in the past 25 years.

“Interchangeability” is an important issue globally that regulators will need to address if patients are to be offered the choice of taking the original biologic drug or substitute a biosimilar drug, just as they currently do with generic versions of chemically synthesized small molecule drugs. U.S. biosimilar regulations have not addressed the issue, while in Europe there are country-specific rules on biosimilar interchangeability.

The lack of clear guidelines on interchangeability with reference biologics is likely to be a cause for concern among physicians until they gain confidence with the usage, experience, and outcomes of biosimilars. However, payers are influencing biosimilar decisions in the U.S. even as the government hashes out guidelines for interchangeability. Leading U.S. pharmacy benefit management (PBM) company CVS Health recently left out Sanofi’s blockbuster insulin glargine product Lantus from its 2017 formulary, replacing it with Eli Lilly and Boehringer Ingelheim’s biosimilar version of Lantus. Such exclusive arrangements could mean deemed interchangeability for the patient subset covered by the PBM.

The naming convention for biosimilars is an issue that needs to be sorted out to ensure that it does not complicate their adoption. The U.S. Food and Drug Administration (FDA) has proposed a four-letter suffix to distinguish between a biosimilar and its reference product, similar to the “biological qualifier” proposed by the World Health Organization (WHO). The first approved biosimilar in the U.S., filgrastim-sndz (Zarxio), had a common United States Adopted Name (USAN) and a suffix (sndz) that reflected the manufacturer (Sandoz). But the second FDA approved biosimilar, infliximab-dyyb (Inflectra), manufactured by Celltrion, was named using a common USAN with an apparently random suffix devoid of meaning. However, the requirement to add a suffix at the end of a biosimilar’s non-proprietary name could lead to confusion among prescribers and patients.

Biosimilar uptake could also see a boost as more regulators back data extrapolation, which will allow a biosimilar to be approved for multiple indications without undergoing clinical testing in those conditions as long as the reference product itself was approved in those conditions.

Stakeholder Education: Need of the Hour

Concerns among health care providers and patients over biosimilar acceptance can only be addressed through stakeholder education. Physicians, patients, and payers require balanced and adequate education on the role that biosimilar medicines can play. Physicians need to be provided data and evidence that biosimilar medicines offer a safe and efficacious alternative to original biologics. Moreover, they also need to be helped to understand the broader clinical and health system benefits of prescribing biosimilar products. Patients need to be reassured that biosimilar products are safe and efficacious. Payers need to be educated about the potential offered by biosimilar medicines in ensuring affordable healthcare. Educating these stakeholders about biosimilar safety and efficacy will likely require cultivating knowledgeable market and opinion leaders. Manufacturers have a key role to play in building trust with these key stakeholders.

Biocon is extending its physician education programs to address the credibility hurdle that needs to be crossed in the minds of biosimilars prescribers. The company organizes an annual breast cancer summit called Converge, which is attended by oncologists from India, Nepal, Sri Lanka, and the Gulf countries. At the event, key opinion leaders (KOLs) share clinical data gathered in real-world settings in order to dispel certain myths associated with the use of biosimilars.

To enhance scientific capability and credibility in the immuno-oncology area, Biocon recently organized an immuno-oncology symposium with eminent scientists such as Prof. Vijay Kuchroo (Harvard), Prof. Gordon Freeman (Harvard), and Prof. Varsha Gandhi (MD Anderson Cancer Center) as key speakers. This was followed by a roundtable discussion, where Indian KOLs in the field presented their perspectives.

Conclusion

These are exciting times for the life sciences sector, as it builds on its understanding of disease at the cellular and genetic level to usher new and differentiated therapies into the market. Furthermore, biomedical advances are likely to transform global health with early diagnosis and therapeutic intervention for chronic and fatal diseases like autoimmune and cancer. The forthcoming generation of biosimilar products will provide affordable access to complex biologics with a promise to enhance the quality of patients’ lives.

Governments in major markets like the EU have recognized the potential financial benefit of biosimilars and are driving their uptake. Besides developed markets like the U.S. and EU, the developing world can also benefit from easier accessibility to these cutting-edge treatments that will lead to better health outcomes. In the coming years, prudent policymaking will be necessary to expand biosimilar volumes and provide patients with greater access to these life-saving drugs.

References:

- Global Use of Medicines in 2020. IMS Institute for Healthcare Informatics, 2016.

- Delivering On The Potential Of Biosimilar Medicines. IMS Institute for Healthcare Informatics, 2016.

- Winning with biosimilars: Opportunities in global markets. Deloitte, 2015.

- Global Biosimilars / Follow-on-Biologics Market. Allied Market Research, July 2014.

- GLOBOCAN 2012: Estimated Cancer Incidence, Mortality and Prevalence Worldwide in 2012, http://globocan.iarc.fr/.

- Global Health Observatory data, WHO.

- Sanford C. Bernstein. Biosimilars: Who Is Doing What?.

- Meek, Thomas. “Nordic Countries Near Complete Switch To Biosimilar Remicade.” APM Health Europe 2016. Sept. 7, 2016.

- Biosimilars Advisory Service: Global Biosimilars Markets, Pipelines, Regulations and Major Players. Decision Resources Group, 2014

- The Economist Intelligence Unit Industry Report, 2014.

- "India Making Strong Progress In Biosimilars, With Local Market estimated at over $9oo million." The PharmaLetter, Feb. 2016.

- Ferreira, Miguel et al. “Unfolding The Biosimilar Landscape In Latin America.” PMLivE, 2013.

About the Author:

Ravindra Kamalakar Limaye is the president of marketing at Biocon. He has over 25 years of experience in the pharmaceutical industry with companies including Novartis, GSK, and Roussel Uclaf (now part of Sanofi). Before joining Biocon, he was responsible for the Novartis Specialty Business Franchise in India, as well as business development and licensing. Prior to that, he spent 14 years at GlaxoSimithKline with responsibilites in India, emerging markets, and Asia Pacific. His diverse roles spanned marketing, sales, business development, corporate strategy, and M&A, including a stint at GSK headquarters in London. Ravindra has a post-graduate degree in pharmacology from University of Mumbai and an MBA from Jamnalal Bajaj, Mumbai.

Ravindra Kamalakar Limaye is the president of marketing at Biocon. He has over 25 years of experience in the pharmaceutical industry with companies including Novartis, GSK, and Roussel Uclaf (now part of Sanofi). Before joining Biocon, he was responsible for the Novartis Specialty Business Franchise in India, as well as business development and licensing. Prior to that, he spent 14 years at GlaxoSimithKline with responsibilites in India, emerging markets, and Asia Pacific. His diverse roles spanned marketing, sales, business development, corporate strategy, and M&A, including a stint at GSK headquarters in London. Ravindra has a post-graduate degree in pharmacology from University of Mumbai and an MBA from Jamnalal Bajaj, Mumbai.

About CPhI Worldwide:

CPhI Worldwide, together with co-located events ICSE, InnoPack, P-MEC, and FDF, hosts more than 37,000 visiting pharma professionals over three days. Over 2,500 exhibitors from more than 150 countries gather at the event to network and take advantage of more than 100 free industry seminars. For more information, visit www.cphi.com/europe.